Loans from the Small Business Administration provide support to millions of entrepreneurs and business owners. You can even use them to fund the outright purchase of an existing business.

When you buy a business rather than starting your own, you can earn money immediately while building on a proven foundation.

It’s a win-win: You get a solid business and a way to pay the funds you used to buy it.

SBA loans slot right into this plan. They give you the funds you need to buy a business and come with long terms and low rates.

Think of it like free money from the government. The government wants to support small business development and growth, and SBA funds make that happen.

Here’s what you need to know about using an SBA loan to fund your goal of buying a business.

The Pros and Cons of SBA Loans

First off, don’t use an SBA loan to buy your very first business. These are non-recourse, personal guaranteed loans. Unless you have a ton of money in the bank, you’re taking the risk of getting deep in debt without an escape plan.

Taking on a complicated loan from the SBA and not understanding how to diversify your risk is one of the quickest ways new business buyers massively f*ck up buying a business.

Long story short, it puts you in the position of taking on a lot of payback risk when you don’t have much experience yet.

But an SBA loan isn’t a bad choice if it isn’t your first business-buying rodeo. You just need to make sure this funding option is the right fit for you.

On the plus side:

- SBA loans come with favorable interest rates and terms.

- You can use the funds for a variety of purposes.

- You can get access to larger capital amounts than many traditional business loans.

- You can tap into support from SBA resource partners to make the application process easier.

The SBA allows borrowers to use funds for things like:

- Short or long-term working capital

- Refinancing any current business debt

- Refinancing, improving, or acquiring real estate

- Complete or partial changes of ownership

- Purchasing supplies, fixtures, or furniture

- Installing or purchasing equipment and machinery

That’s a pretty broad list of potential uses. It’s no surprise plenty of would-be business owners turn to the SBA when trying to buy a business.

But it’s not all sunshine and rainbows.

Here are some of the biggest downsides of applying for an SBA loan:

- The SBA has a rigorous application process, which can feel overwhelming.

- There are strict qualification criteria in place with no wiggle room.

- You might face longer approval times when compared with the traditional lending process.

Getting a traditional bank loan is bad enough. Add government approval into the mix and you’re in for a long and bureaucratic process.

And that’s if you qualify for an SBA loan in the first place.

Who Qualifies for an SBA Loan for Business Acquisitions?

SBA loans are very popular because of their terms, but not everyone qualifies to get one.

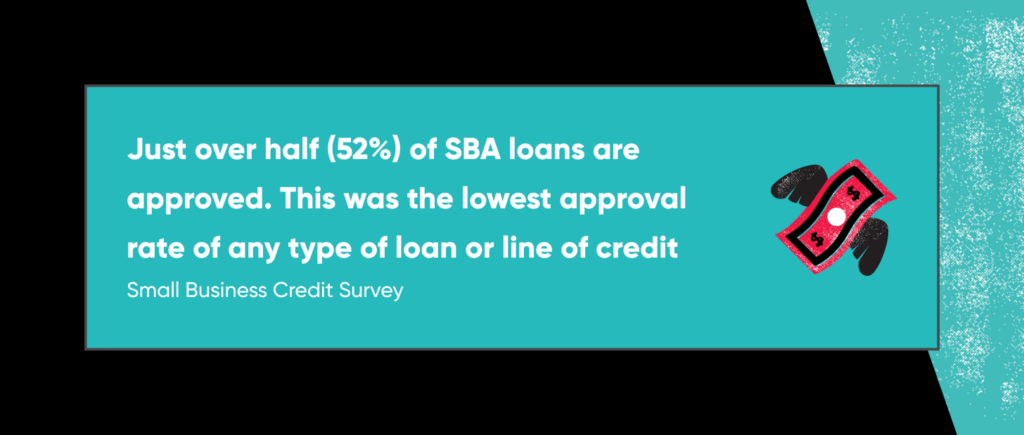

Lenders only approve around half of SBA loan applications. You’ll need a strong application and double-check your eligibility to get the funds you need.

Eligibility cuts both ways: The SBA looks at both borrowers and the business.

Borrower Eligibility

Here’s the rundown of the must-haves for the business owner’s SBA loan application:

- A FICO score of 690 or above for all business owners

- Some type of personal or business collateral to secure part of the loan

- Some industry or managerial experience

- A 10% down payment

- No criminal history

- No other federal debt

- No bankruptcies on your record in the past 3 years

- Be unable to secure financing from non-federal, non-state, and non-local government sources

- For partial ownership changes, the applicant’s debt-to-worth ratio cannot exceed 9:1

You can use things like real estate, vehicles, or equipment as collateral. Just know that your lender might discount the value you place on collateral due to depreciation.

Business Eligibility

The business itself needs to meet certain criteria, too. The business must:

- Meet the SBA definition of small business

- Have at least 2 years of operational history as a registered, for-profit company

- Operate within the U.S. or its territories

Whether or not the SBA considers the business a “small business” depends on:

- The number of employees working for the business

- The average annual receipts (which include gross income and the “cost of goods sold” listed on the company’s tax returns)

For example, a roofing contractor making more than $19 million in annual receipts is not a small business.

The SBA breaks 100s of different types of business down into categories in the North American Industry Classification System (NAICS). Each industry has its own NAICS code and a standard size that the SBA defines.

Look up the NAICS code for the type of business you want to buy. Choose the number that best describes what the company does.

Once you find the code that matches the business, check the SBA’s standard sizes to see if the business is below the administration’s threshold.

The SBA will also request a range of financial documentation before approving your application.

Be prepared to submit any of the following with your loan application:

- 6 months of business bank statements

- At least 2 years of business tax returns

- Month-to-date transactions

- Any debt schedules

- 2 years of personal tax returns for anyone who will have 20% or more ownership stake

- Year-to-date profit and loss statement

- Year-to-date balance sheet

- Voided check from the business bank account

The SBA offers this checklist for 7(a) loans, but they may require other documents as you work your way through the process.

How to Get an SBA Loan to Buy a Business

You’re ready to start applying for your loan once you’ve checked your eligibility and made sure the business you want to buy qualifies.

Follow the steps below to apply for an SBA loan.

Note: Most people who get to the point of looking into SBA loans already know what kind of business they want to buy. Having a clear set of goals makes it much easier to fill out the application.

If you’re not sure what kind of business you want to buy, we recommend checking out our guide to buying a business before moving on.

Step 1: Determine What Kind of SBA Loan You Need

There are 3 main types of SBA loans to choose from when you buy a business:

- SBA 7(a) loans, which allow you to borrow a maximum of $5 million

- SBA 504 loans, which fund large equipment and real estate purchases

- SBA microloans, which provide up to $50,000 in funding

SBA 7(a) loans are the gold standard because of the high potential lending amounts and decent terms. They’re especially nice for an owner who would otherwise not qualify for traditional lending.

You can use them for up to 10 years for working capital and up to 25 years for fixed assets.

The more details you have about the company you want to purchase, the easier it is to determine which SBA loan lines up.

Step 2: Find SBA-Approved Lenders

It’s a common misconception that you get funds straight from the SBA by submitting an application to them.

Instead, you need to obtain approval from both the SBA and an approved lender.

The majority of 7(a) lenders are banks, including both regional banks and national brands.

But 504 lenders and microloan lenders vary from one region to another. You can find small loans from local banks or through a non-profit lending organization the SBA calls a Certified Development Company.

What you need to know is that many of these lenders set their own application requirements. In some cases, they set the rates for the loan (up to the SBA’s maximum).

You need to do your research to find the best lender for your needs. Check out the SBA lender match tool to start that process.

Step 3: Prepare a Comprehensive Loan Application

The lender you choose will let you know what financial documents they need in your application. Be prepared to include any of the following in your application:

- The business’s bank statements

- The business’s tax returns

- A log of month-to-date transactions

- Any debt schedules

- A year-to-date profit and loss statement

- A year-to-date balance sheet

- A voided check from the business bank account

- Personal tax returns for anyone who will have 20% or more ownership stake

You’ll need 3 more things in addition to the financial documentation:

- Copies of business licenses/certificates

- A business plan

- Details about the business principals

The business plan is crucial for illustrating that you have a solid strategy. It should include:

- An overview of the business history

- The desired loan amount and term

- What you hope to do with the funds

- How you’ll repay the funds

Include the resumes of any owners of the business along with the application.

Combine all this information with your purchase agreement and submit it to the lender.

Step 4: Navigate the Approval Process

The lender will look at your full application package to determine if they want the SBA to guarantee it.

If the lender approves your application, they’ll send it to the SBA for review.

Don’t expect this smooth sailing in this phase. This process takes time, even if you put a lot of effort into your application.

Lenders always have questions, and most will ask for more materials from you.

This is normal. Continue to communicate with them.

Note that the most common reasons for loan denial include:

- Not enough collateral

- Not enough time in business

- Poor cashflow

- An unimpressive business plan

- Financial statement issues, such as gross margin problems or balance sheet mismatch

This is why it’s so important to do your due diligence before considering any financing. If you follow a checklist for buying a business, you’ll know long before creating a loan application whether a business has poor cashflow or finances that don’t make sense.

And, if you’re worried about things like collateral getting in the way of your loan, check out our guide to buying a business with no money.

Step 5: Finalize the Purchase and Transfer Ownership

It can take anywhere from 7 to 14 days after the lender and SBA approve your application to get your funds.

Once you get the money, you can make your payment to the business owner. You’ll be able to start transferring the business (and all of its assets) into your name.

Here are a few things to consider as you enact your takeover plan:

- Try to keep the existing owner in place for a time to ensure you’ve dealt with all questions and have a clear roadmap for the days ahead.

- Move over all certificates, licenses, insurance policies, and software contracts to your name as soon as possible.

- Set yourself up to make regular repayments to the SBA.

Alternatives to SBA Loans for Business Acquisitions

While it’s awesome to grab that government money when you can, SBA loans are truly just one option for buying your dream boring business.

If they’re not a fit for you, if this is your first biz buy, or if the lender declines your application, here are some other ways to finance a business purchase:

- Personal savings (private loans, selling assets, savings, tapping into credit).

- Raising investment funds (by giving out equity in the company).

- Traditional business loans from lenders not affiliated with the SBA.

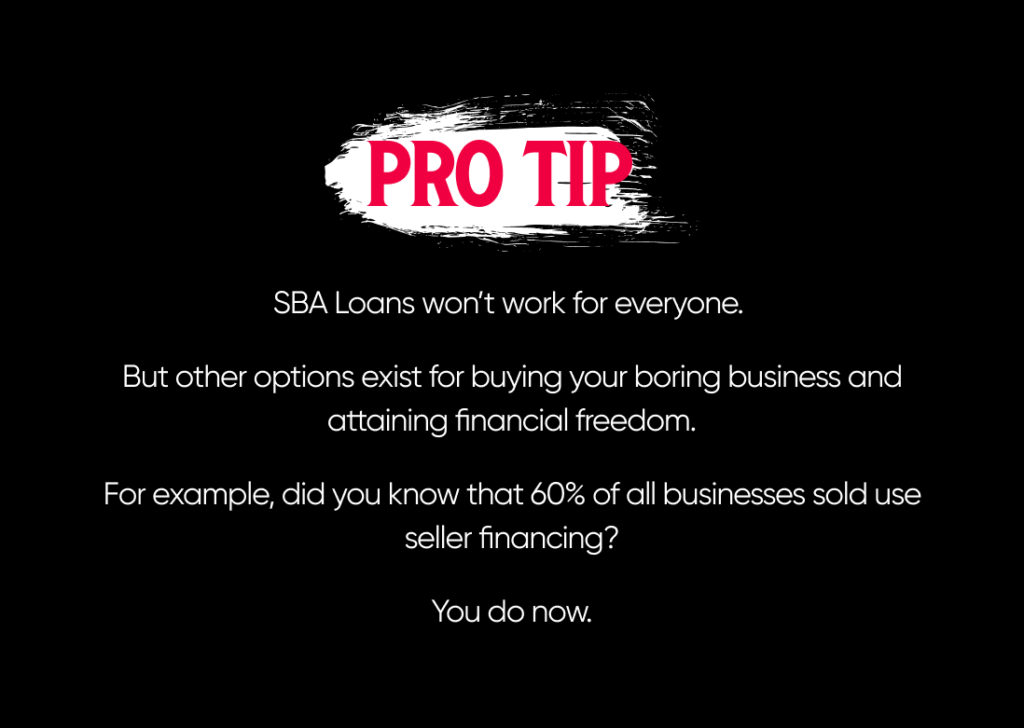

- Seller financing (working out a deal with the seller for a down payment and a payback period).

Here’s a quick breakdown of those options:

| Funds Source | What to Know |

| Personal savings | Hard to get enough funds to buy a full-on business, and risky to put all your eggs in one basket. You could use up all your cash and credit reach pretty quickly, leaving you stuck until the new biz makes a profit. |

| Investor funds | Have to give up equity in your own business, which could limit future profits. |

| Traditional business loans | Just as much red tape as SBA loans and long approval times. May have stricter requirements (like higher credit scores). |

| Seller financing | May have to haggle back and forth with the seller to get agreed-on terms, but usually more flexible than a bank loan. You control the terms here but need good negotiation skills. |

It’s Time to Fund Your New Business Buy

Buying a business calls on you to keep track of a lot of moving parts.

Put in the work upfront with proactive research and exhaustive due diligence to make sure you’re in the best position possible for an SBA loan approval if you go that route.

If you can, consider seller financing instead of an SBA loan or as a backup plan.

SBA loans are not bad if that’s the best you can do, but seller financing opens the door to more creative deal terms. As an added bonus, the previous owner keeps a vested interest in the company’s success with seller financing, which can give you a confident kickstart as the new owner.